What Is a Potentially Exempt Transfer (PET)?

Taper relief only applies to lifetime gifts known as Potentially Exempt Transfers (PETs). These are gifts of assets (cash, property, shares, etc.) made by an individual to another individual.

At the time of the gift, it’s tax-free, but only if the person survives for seven years after making it. If they die within that time, the value of the gift is brought back into their estate for inheritance tax (IHT) purposes.

However, this is where taper relief comes in.

How Taper Relief Works

If the donor dies within seven years of making the gift, inheritance tax may apply. But from year three onwards, taper relief starts to reduce the amount of tax payable on the gift.

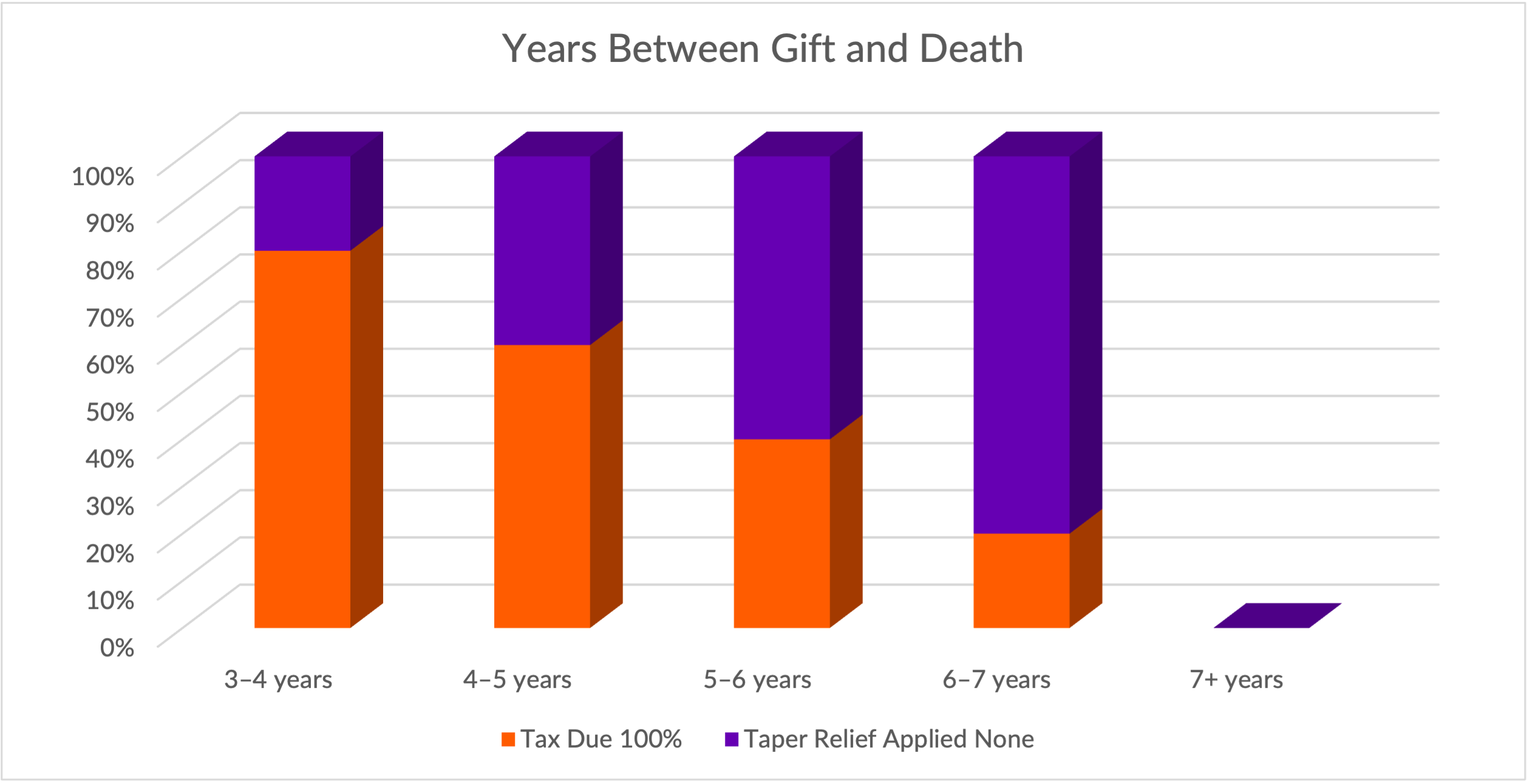

Here’s the sliding scale:

| Years Between Gift and Death | Tax Due | Taper Relief Applied |

|---|---|---|

| 0–3 years | 100% | None |

| 3–4 years | 80% | 20% |

| 4–5 years | 60% | 40% |

| 5–6 years | 40% | 60% |

| 6–7 years | 20% | 80% |

| 7+ years | 0% | Full exemption |

So, while you don’t get total exemption until year 7, even surviving four or five years can result in significant tax savings.

Important Distinction: PETs vs. Trusts

Taper relief applies only to PETs, gifts made to individuals. It does not apply to gifts into discretionary trusts, which are chargeable lifetime transfers (CLTs).

Trusts follow different rules and could trigger an immediate 20% charge over the nil-rate band.

Example: How Taper Relief Saves Money

Sarah gifts £500,000 to her daughter in June 2018. She passes away in August 2023.

- That’s 5 years and 2 months, so taper relief applies.

- £500,000 – £325,000 (nil-rate band) = £175,000 potentially taxable

- Normal IHT rate: 40% → £70,000

- Taper relief (60%) reduces tax due to £28,000

Without taper relief, her estate would owe £70,000. But because she survived more than 5 years, the family saved £42,000.

The 14-Year Rule – A Complication to Know

There’s a 14-year rule that can make things trickier. If the person made gifts into trusts within seven years before making a PET, and dies within seven years of the PET, the trust gifts are also counted.

This rule doesn’t affect most people, but for those with complex estate planning strategies, it’s worth getting advice to avoid nasty surprises.

Practical Tips for Using Taper Relief

- Start gifting early: The earlier you begin, the more likely taper relief will apply.

- Track your gifts: Keep detailed records of what was given, to whom, and when.

- Ensure gifts are outright: To qualify as a PET, gifts must have no strings attached (e.g., you can’t give your home but keep living in it).

- Don’t exceed the nil-rate band without a plan: Be strategic in how you gift to manage exposure.

Who Should Consider Taper Relief?

- Individuals with estates over £325,000 (or £500,000 including the main residence nil-rate band)

- Families with large property, shareholdings, or savings

- Parents or grandparents looking to pass on wealth tax-efficiently

If you’re thinking long term, and want to avoid a 40% hit to your family’s inheritance, taper relief should be part of your strategy.

Talk to Our Estate Planning Experts Today

Taper relief is one of those tax rules that sounds simple, but has layers of nuance. Used right, it’s a powerful tool to reduce IHT. Used wrong, and you might leave your family with a bill that could have been avoided.

That’s where we come in.

Our estate planning team can:

- Map out your PETs and gifting strategy

- Estimate future IHT exposure

- Help structure your estate to minimise tax

Frequently Asked Questions: Taper Relief and Inheritance Tax

Q1: What is taper relief in inheritance tax?

Taper relief reduces the amount of inheritance tax due on certain lifetime gifts if the person who made the gift dies between three and seven years after giving it.

Q2: When does taper relief start to apply?

Taper relief starts to apply after three years from the date the gift was made. No relief is available if the person dies within the first three years.

Q3: Does taper relief reduce the value of the gift?

No. Taper relief does not reduce the value of the gift itself. It only reduces the inheritance tax payable on that gift if tax is due.

Q4: Does taper relief apply to all lifetime gifts?

No. Taper relief only applies to Potentially Exempt Transfers (PETs), which are gifts made to individuals. It does not usually apply to gifts made into trusts.

Q5: Can taper relief reduce inheritance tax to zero?

Yes. If the person who made the gift survives seven years or more, the gift becomes fully exempt from inheritance tax and no tax is due.

Ready to Plan for Your Future?

Book a discovery call to chat through how Estate Planning could unlock your next stage of growth.

Want to read more? Click here for more Nuvo blogs

Recent Posts / View All Posts